Risk Strategy

What Is Risk Governance? (And Why It Matters More Than Your Risk Register)

Risk governance is the operating layer that turns risk information into executive decisions. The 5 components every mid-market governance structure needs, where Fortune 500 models fail at $50M to $500M scale, and a 60-day path to building governance that works.

By Eric Kennedy · Wed Jun 03 2026 · 8 min read

TL;DR: Risk governance is the system that decides how risk information moves through an organization and how it influences executive decisions. It is not a risk register, it is not a heat map, and it is not internal audit. It is the operating layer that connects what the organization knows about risk to what the organization actually does about it. At a mid-market company, risk governance is the difference between a polished ERM artifact that sits on a shared drive and a working program that earns its place at the capital allocation conversation. This guide covers what risk governance actually is, the 5 components every mid-market governance structure needs, where Fortune 500 governance models fail when applied at $50M to $500M scale, and a practical path to building governance that works at your size.

A mid-market CFO who has built a risk register, run a workshop, and produced a heat map has not built risk governance. They have built risk documentation.

The distinction matters because it determines whether the program produces decisions or paper.

Risk governance is the discipline of deciding, in advance, how risk information moves through the organization, who owns it at each stage, what triggers escalation, and how the picture connects to executive decision-making. The register, the heat map, the workshop, none of those are governance. They are inputs. Governance is the operating system that turns those inputs into action.

Most mid-market ERM programs have built the inputs and stopped there. This article covers what risk governance actually is, why the mid-market context is different from Fortune 500, the 5 components every working governance structure needs, and how to build one that produces value at your scale.

What risk governance actually is, and what it isn't

Risk governance is the framework of accountability, decision rights, and reporting structures that determines how an organization manages risk over time. It defines who owns what, when escalation happens, where the risk picture goes, and how the conversation connects to the rest of the business.

That's the definition. Now what it is not.

Risk governance is not a risk register. A register lists risks. Governance decides what happens to them.

Risk governance is not a heat map. A heat map is one output. Governance is the system that produces it, updates it, and acts on it. (More on building a heat map that drives decisions.)

Risk governance is not internal audit. Audit tests whether controls work. Governance decides which risks need controls in the first place.

Risk governance is not compliance. Compliance manages a specific subset of risk against external requirements. Governance covers the full risk picture and decides what to do with it strategically.

Risk governance is not an ERM software platform. Software is a tool. Governance is the structure the tool serves.

The shorthand: governance is the operating layer. Everything else is documentation, instrumentation, or output.

Why mid-market governance is different from Fortune 500

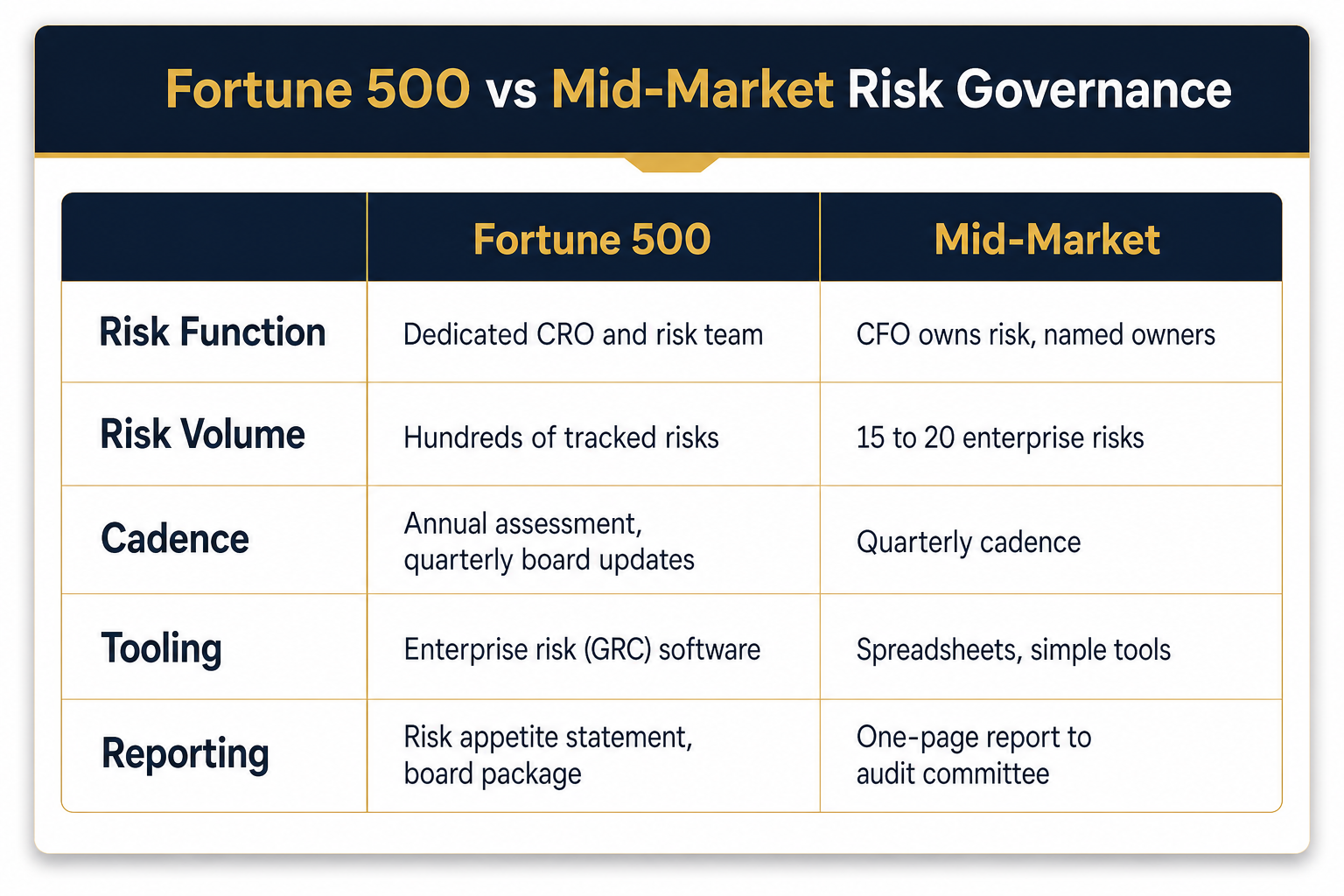

Most published guidance on risk governance assumes a Fortune 500 operating context. That context has a chief risk officer, a board-level risk committee, a dedicated risk committee charter, multiple risk subcommittees by function, and an ERM software platform that integrates risk reporting across business units.

At a mid-market company, none of that exists, and trying to build a smaller version of it is one of the most common reasons mid-market ERM programs fail.

The Fortune 500 governance model assumes scale that mid-market companies do not have. The 2025 Deloitte and Center for Audit Quality Audit Committee Practices Report (4th edition) shows that even among large public companies, only 19% have a dedicated risk committee at the board level. The audit committee owns ERM oversight in 52% of cases, with the full board owning it in another 28%. The picture changes by industry: 48% of financial services companies use a dedicated risk committee, but only 8% of non-financial services companies do.

For mid-market companies specifically, the BDO 600 2025 Board Compensation Survey of public mid-market companies (revenues $100M to $4.5B) found that only 10% maintain a dedicated risk committee. The other 90% allocate risk governance to the audit committee, the full board, or a hybrid arrangement.

This is the structural reality mid-market governance has to work within: no CRO, no dedicated risk committee, no enterprise risk software, an audit committee that meets four times a year, and a CFO who owns risk in addition to finance, treasury, and FP&A.

A working mid-market risk governance structure is not a smaller version of the Fortune 500 model. It is a different operating model that uses different mechanisms to accomplish the same outcomes: decision rights, escalation paths, reporting cadence, and accountability for the risks that matter most.

The 5 components of a working mid-market governance structure

A working risk governance structure at a mid-market company has five components. Each component answers a specific question about how risk moves through the organization. Without all five, the structure is incomplete and produces documentation rather than decisions.

- Decision Rights. Who decides what, and at what level? At a mid-market company, the CFO typically owns the risk function operationally, the CEO owns strategic risk decisions, and the audit committee owns oversight. The boundaries between those three need to be defined explicitly, not implied. The most common failure mode is a CFO who runs the register but does not have explicit authority to escalate to the board, which means material risks stall at the management layer.

- Risk Ownership. Every material risk needs a named owner accountable for monitoring, reporting, and escalation. Not a department. Not a committee. A person. The risk owner is responsible for surfacing changes between formal review cycles, recommending response actions, and reporting status to the CFO each quarter. (This is one of the four gaps that breaks mid-market ERM programs.)

- Cadence. Risk governance runs on a defined rhythm: quarterly business-unit-level reviews, quarterly CFO consolidation, semi-annual audit committee briefings, and annual board-level reporting. The cadence is the mechanism that keeps the risk picture current. Annual-only cycles fail because the risk environment changes faster than the cycle.

- Escalation Paths. When a risk moves materially, when a vendor fails, a key person departs, a regulatory change lands, an assumption breaks, governance defines how that information travels from the operational level to the decision layer. Escalation paths need explicit triggers (what counts as material), explicit routing (where it goes), and explicit response (what happens within how many hours). Without defined escalation, known risks stay known at the wrong level of the organization. (Most mid-market companies miss this entirely.)

- Reporting and Connection to Decisions. The risk picture has to reach the people making capital allocation, strategic, and operational decisions in a format they can use. A 40-page risk report does not do that. A one-page quarterly summary with the top 5 risks, their status, and the decisions the leadership team needs to make does. According to the AICPA and NC State 2025 State of Risk Oversight Report, only 30% of organizations integrate risk exposure into capital allocation decisions. That is the moment governance either earns its place or becomes overhead.

What gets governance wrong at mid-market

When the Fortune 500 governance model gets applied at mid-market scale, it breaks in four predictable ways. Each one is diagnosable and fixable.

Failure 1: No explicit decision rights. Decision authority is implied rather than documented. The CFO assumes they can escalate. The CEO assumes the CFO will tell them when something material happens. The audit committee assumes someone is bringing them the right things. None of those assumptions are wrong individually. Together, they produce a system where material risks stall because no one is sure they have authority to act. The fix: a one-page decision rights document, approved by the CEO and audit committee chair, that names who decides what at what threshold.

Failure 2: Governance assigned to the wrong body. At many mid-market companies, ERM oversight gets handed to the audit committee by default. That is appropriate for non-financial services companies (where 63% of non-FS organizations follow this model per Deloitte/CAQ 2025) but the assignment needs to be deliberate, not automatic. The audit committee charter should explicitly include ERM oversight, with time on the agenda each quarter, and the chair should be briefed between meetings on material developments. Otherwise the responsibility exists on paper and nowhere else.

Failure 3: No mechanism for between-cycle escalation. Quarterly cadence works for steady-state risk monitoring. It fails when a material risk emerges between cycles and there is no defined path to surface it. A vendor failure, a regulatory action, a key person departure, a customer concentration shift, all of these need to reach the CFO within hours and the audit committee chair within days, not at the next quarterly review. Most mid-market governance structures have no defined between-cycle escalation protocol, which means material risks wait three months for visibility.

Failure 4: No connection to capital allocation. Per the AICPA and NC State 2025 data, only 30% of organizations integrate risk into capital allocation decisions. This is the most consequential failure because it is where governance either earns its place at the executive table or becomes a parallel track. The fix is structural: the quarterly risk report becomes one of the inputs to the leadership team's capital allocation conversation. Not a separate meeting. Not a separate process. The CFO connects the dots out loud, every quarter.

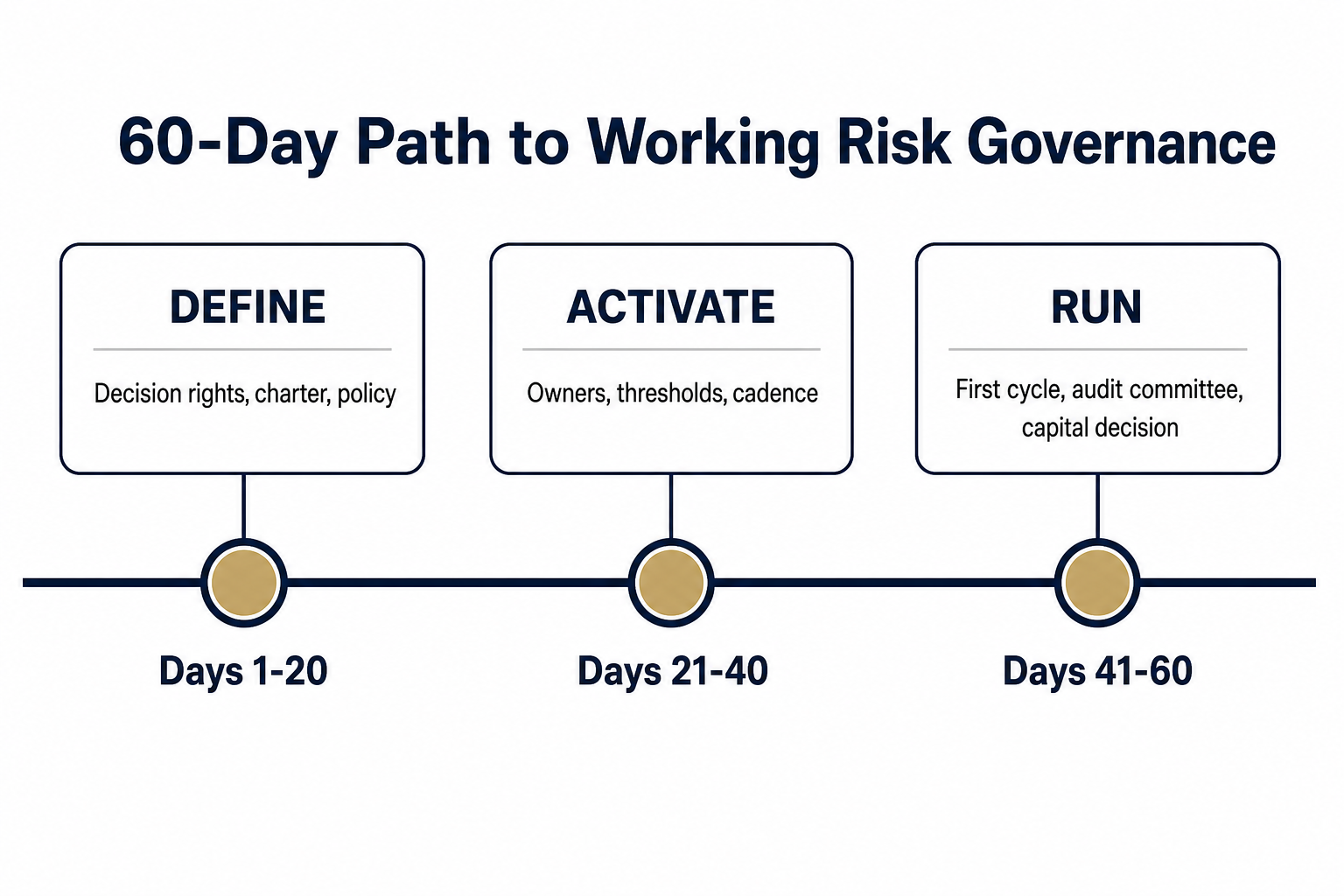

A 60-day path to working risk governance at mid-market

For a mid-market company building risk governance for the first time, or rebuilding from a broken program, here is a realistic 60-day path.

Days 1 to 20: Define the structure. Document the decision rights between CEO, CFO, and audit committee. Update the audit committee charter to explicitly include ERM oversight. Draft a risk governance policy (one to two pages) that names who owns what, what triggers escalation, and how reporting flows. Get audit committee chair and CEO buy-in.

Days 21 to 40: Activate the components. Name owners for the top 15 to 20 enterprise risks. Define escalation thresholds and routing. Design the one-page quarterly risk report template. Schedule the quarterly governance cadence: business unit reviews, CFO consolidation, audit committee briefings.

Days 41 to 60: Run the first cycle. Execute the first quarterly review with the leadership team. Brief the audit committee using the new format. Connect the risk picture to at least one capital allocation decision in the same cycle. Adjust the structure based on what worked and what did not.

At 60 days, you have a working risk governance structure. Not a Fortune 500 governance model. A working mid-market structure that produces real decisions on a real cadence, with named accountability and a defined connection to executive decision-making.

Why this matters more than your risk register

A risk register is an inventory. Risk governance is what you do with the inventory.

The AICPA and NC State 2025 data captures the gap precisely: only 35% of organizations have comprehensive ERM processes in place, and only 11% see their risk management process as a strategic competitive advantage. The remaining majority are running risk documentation, not risk governance.

The mid-market companies that get the most value from ERM are not the ones with the most polished registers. They are the ones whose governance structure actually connects risk awareness to executive decisions, on a cadence that keeps the picture current, with named owners who are accountable for what changes.

The register is solved. Most companies have one. The governance is the work.

Key Takeaways

- Risk governance is the operating layer that decides how risk information moves through the organization and how it influences executive decisions. It is not a risk register, a heat map, or internal audit.

- Mid-market risk governance is not a smaller version of the Fortune 500 model. Only 10% of mid-market public companies maintain a dedicated risk committee (BDO 600 2025); 90% allocate risk oversight to the audit committee, the full board, or a hybrid.

- A working mid-market governance structure has five components: decision rights, risk ownership, cadence, escalation paths, and reporting connected to decisions.

- Four governance failures consistently break mid-market programs: no explicit decision rights, governance assigned without intent, no between-cycle escalation, and no connection to capital allocation.

- 60 days is enough to stand up a working risk governance structure: 20 days of definition, 20 days of activation, 20 days of first-cycle execution.

- Only 30% of organizations integrate risk into capital allocation decisions (AICPA/NC State 2025). That is the moment governance either earns its place or becomes overhead.

Where to Start {eyebrow="BUILD THE OPERATING LAYER"}

If your organization has a risk register but not the governance structure underneath it, the answer is not better documentation. It is a deliberate build of the operating layer: decision rights, named owners, defined cadence, escalation paths, and direct connection to executive decisions.

ERM Foundation Build{.cta-primary} ERM Diagnostic{.cta-secondary}

The ERM Foundation Build (8 to 12 weeks) is KRG's flagship engagement for organizations ready to build the governance layer underneath their ERM program. We document decision rights, name owners, define escalation thresholds, stand up the quarterly cadence, and run the first cycle with the leadership team and audit committee. If you want a maturity assessment first, start with the ERM Diagnostic. The diagnostic fee is credited toward the Foundation Build if you move forward.

Frequently Asked Questions

What is risk governance in simple terms?

Risk governance is the structure that defines how an organization makes decisions about risk. It includes who owns each risk, who decides what at what level, when risks escalate, how often the picture gets reviewed, and how the risk view connects to executive decisions about capital, strategy, and operations. Risk governance is the operating layer of an ERM program; risk registers and heat maps are outputs of that operating layer.

How is risk governance different from risk management?

Risk management is the broader discipline of identifying, assessing, and responding to risk. Risk governance is the subset of risk management that handles accountability, decision rights, and reporting structures. You can practice risk management at a tactical level without risk governance, but the result is documentation rather than a program that drives decisions. Governance is what makes risk management durable and connected to executive decision-making.

Who is responsible for risk governance at a mid-market company?

At most mid-market companies, the CFO is the operational owner of risk governance, the CEO owns strategic risk decisions, and the audit committee provides board-level oversight. According to the 2025 Deloitte and CAQ Audit Committee Practices Report, 52% of audit committees own ERM oversight at a board level, with the full board owning it in another 28% of cases. Among mid-market public companies specifically, only 10% have a dedicated risk committee (BDO 600 2025), so audit committee or full-board oversight is the dominant model.

What is the difference between an audit committee and a risk committee?

An audit committee oversees financial reporting, internal controls, external audit, and (in most non-financial services companies) ERM. A risk committee is a dedicated board committee focused exclusively on enterprise risk oversight. Risk committees are common in financial services (48% of FS companies have one per Deloitte/CAQ 2025) and rare in non-financial services (only 8%). Among mid-market public companies broadly, only 10% maintain a dedicated risk committee. For most mid-market companies, the audit committee is the appropriate home for risk governance oversight, with the charter explicitly extended to cover ERM.

How often should risk governance review risks?

A working mid-market risk governance structure operates on a quarterly cadence at the business unit and CFO consolidation level, with semi-annual audit committee briefings and annual board-level reporting. Material developments between cycles trigger explicit escalation, with defined routing to the CFO within hours and the audit committee chair within days. Annual-only review cycles fail because the risk environment changes faster than the cycle. Quarterly is the minimum for keeping risk intelligence current.