Risk Strategy

Strategic Risk Management for Mid-Market CFOs: What It Actually Means in Practice

Strategic risk management for mid-market companies is a different operating model from the Fortune 500 version. A short list of named risks, one owner each, a quarterly cadence, and a one-page report.

By Eric Kennedy · Tue May 12 2026 · 8 min read

TL;DR: Strategic risk management for mid-market companies is a different operating model from the Fortune 500 version. Effective programs have three properties: a short list of 20 to 40 named strategic risks, one designated owner per risk, and a quarterly cadence integrated into the existing finance operating rhythm. The CFO role in risk management at the mid-market level is integration, not ownership. The result: faster risk-informed decision making and decisions that actually happen.

If you are a mid-market CFO and you have read three different articles about strategic risk management, you have probably noticed they all describe the same company. That company has a Chief Risk Officer reporting to the CEO. It has a dedicated enterprise risk team. It has a formal risk appetite statement approved by the board. It has quantitative risk models running scenarios across a multi-billion-dollar P&L.

Your company does not look like that. It probably never will.

This is the problem with most strategic risk management content. It describes the Fortune 500 operating model and assumes the mid-market version is a smaller copy. It is not. The mid-market version is a different operating model entirely, one that produces the same outcomes with less infrastructure. Effective risk management strategies for mid-market companies do not scale down from the Fortune 500 playbook. They are built differently from the start, with the CFO role in risk management positioned as the integration point rather than as the owner of an enterprise risk management framework built for a much larger company.

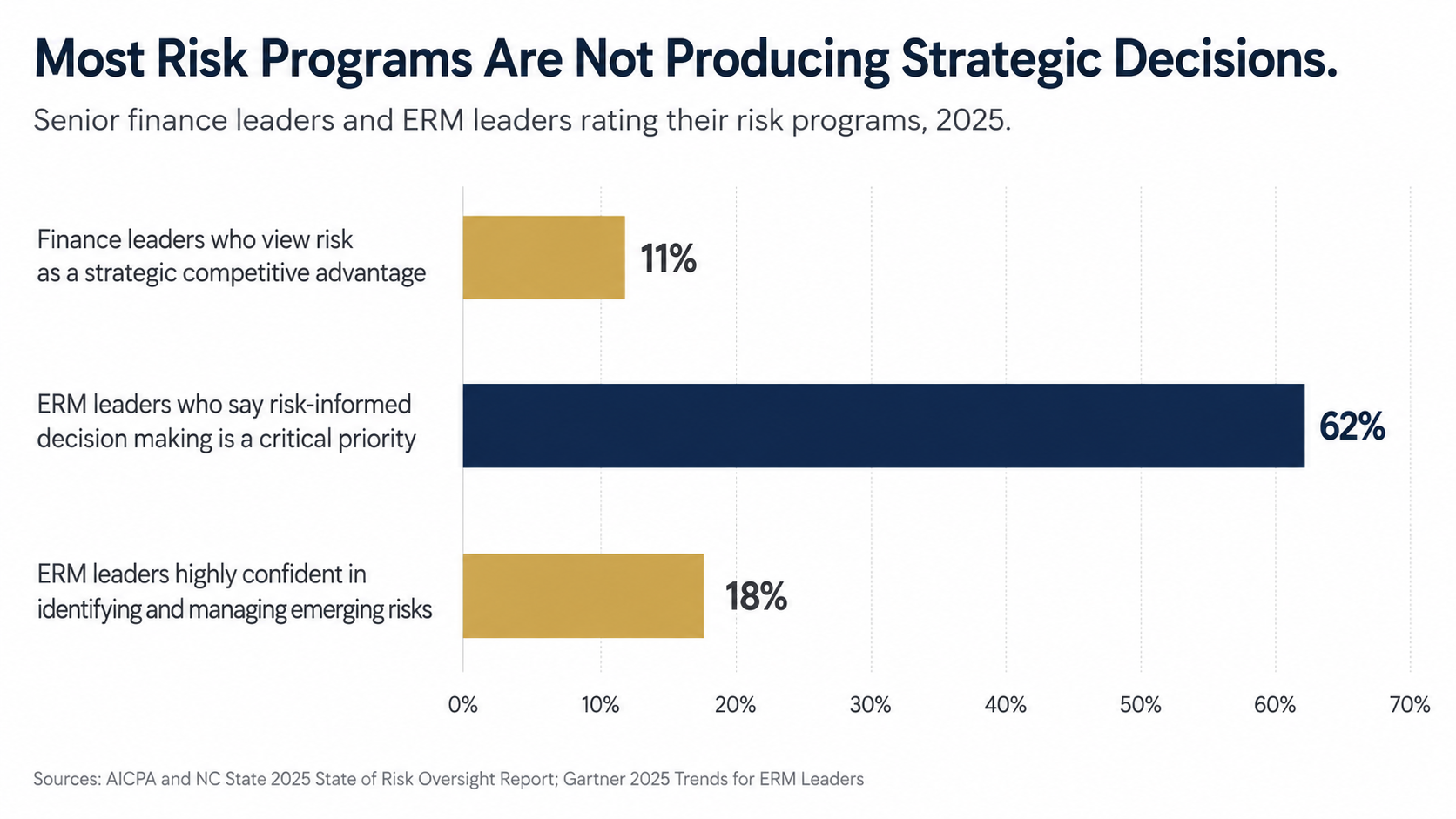

The data confirms why this matters. The AICPA and NC State 2025 State of Risk Oversight Report found that only 11% of senior finance leaders view their organization's risk management process as "mostly" or "extensively" a strategic tool that delivers competitive advantage, with 64% saying it provides no or minimal advantage. Strategic risk management is failing at most companies, regardless of size. The cause is structural, not effort-related, and the fix at the mid-market level looks different from the Fortune 500 fix.

What strategic risk management actually means

Strip out the jargon and strategic risk management is straightforward. It is the discipline of identifying the risks that could prevent the company from achieving its strategy, owning them at the executive level, monitoring them on a known cadence, and escalating them when they move.

Four parts. Identification. Ownership. Monitoring. Escalation.

A Fortune 500 company builds elaborate infrastructure around each of these. A CRO function manages identification. The audit committee owns it at the board level. A team of analysts monitors using quantitative models. A formal escalation framework determines when risks reach the board.

A mid-market company needs the same four parts. It does not need the infrastructure. What it needs is a different operating model.

Why the Fortune 500 model breaks at the mid-market

Three reasons.

Headcount. A $250M company does not have a CRO. It does not have a risk committee staffed by independent directors. It probably does not even have a dedicated risk function. Trying to replicate a CRO-led model means asking the CFO, controller, or general counsel to add a major function to an already full role.

Risk volume. A Fortune 500 company tracks 200 to 500 enterprise risks because it has the operational complexity to justify that many. A $200M company has 20 to 40 risks that actually matter at the executive level. Building a 200-row risk register at that scale is busy work that obscures the risks that count.

Cadence. Fortune 500 risk programs run a multi-week annual risk assessment with hundreds of interviews. According to the same AICPA report, 61% of finance leaders acknowledge that risk volume and complexity have changed "mostly" or "extensively" over the past five years, but only 35% report having comprehensive ERM processes in place. Mid-market companies cannot run a months-long assessment annually. They need a quarterly rhythm that updates the risk picture in a few hours of executive time.

The Fortune 500 model is right for Fortune 500 companies. It does not scale down to mid-market because the bottleneck is not the framework. The bottleneck is executive time.

What effective risk management strategies look like at the mid-market

Three properties define an effective mid-market strategic risk management program.

A short, named list of strategic risks. Not 200. Not 100. Usually 20 to 40 enterprise-level risks, each one named at a level the executive team would actually recognize and discuss. "Customer concentration in top three accounts" rather than "Revenue dependency risk." "Cyber breach of customer data" rather than "Information security risk." The naming convention matters because the list has to be usable in a 20-minute executive review.

One designated owner per risk. Not a committee. One person. Usually a member of the executive team or the next layer down. The owner is responsible for monitoring the risk, knowing the current state, and bringing it to the CFO or audit committee when it moves. Gartner's data underscores why ownership matters: only 18% of risk owners provide high-quality information about their risks, and just 14% have effective mitigation plans. If a risk does not have one named owner, it does not have any owner.

A quarterly cadence integrated into the existing finance operating rhythm. Not a separate process. A 30-minute segment in the existing quarterly executive review. Each owner provides a one-line update on their risks: current state, trend, action this quarter. The CFO or risk owner consolidates the updates into a one-page risk report for the audit committee.

That is strategic risk management at the mid-market level. Twenty to forty risks, one owner each, a quarterly rhythm, a one-page report. No CRO required. No dedicated risk committee required. No quantitative modeling required.

The CFO role in risk management: connecting strategy, finance, and governance

The mid-market integration question is where most programs break down. Strategic risk management cannot live as a separate process owned by a part-time risk lead. It has to integrate with the CFO's finance operating rhythm and with the audit committee's governance cadence, or it becomes a third stream of work that nobody actually uses.

Three integration points do most of the work.

Finance integration. The quarterly risk update sits inside the existing finance quarterly review, not as a separate meeting. Risk owner updates feed into the same cycle that produces the CFO's executive financial commentary. This is the single most effective way to keep the program alive once the initial build is done.

Governance integration. The audit committee receives one consolidated one-page risk report as part of the standard audit committee package, not as a separate strategic risk submission. The CFO role in risk management at this level is integration: making sure the audit committee sees risk alongside the financial and audit topics they already review.

ERM framework integration. Strategic risk management is the top layer of a broader enterprise risk management framework that includes operational risk, compliance risk, and internal audit findings. At the Fortune 500 level these are separate workstreams. At the mid-market level they share one risk register, one owner list, and one report. That is what makes the model work, and it is the foundation of KRG's ERM Foundation Build engagement.

Two strategic risk management examples at the mid-market

Two strategic risk management examples make the model concrete. These are not Fortune 500 hypotheticals. They are how mid-market companies actually run risk-informed decision making in practice.

Example 1: A $200M industrial distributor with customer concentration. The top three accounts represent 47% of revenue. The strategic risk is named "Concentration in top three accounts," owned by the Chief Revenue Officer. Each quarter, the CRO reports the concentration percentage, any change in account health, and the diversification action this quarter. The CFO consolidates and the board sees a single line: "Concentration steady at 47%, no health signal change, account diversification pipeline at $X." That is strategic risk management. No CRO function. No risk modeling. One owner, one quarterly update, one decision-ready line for the board.

Example 2: A $300M software company with regulatory exposure. The strategic risk is named "State privacy law compliance gap," owned by the General Counsel. Each quarter, the GC reports the number of states where the company has obligations, any new state legislation in scope, and the compliance action this quarter. When Connecticut lowered its in-scope threshold in 2025, the GC flagged it in that quarter's update and the CFO redirected $40K of budget to close the gap. That decision happened because the risk had a name, an owner, and a recurring update slot. Fortune 500 ERM programs often do not produce decisions that fast.

Why this produces better decisions than larger programs

The Fortune 500 model often fails not because it lacks rigor but because the rigor disconnects from decisions. Gartner found that 62% of enterprise risk management leaders agree that risk-informed decision making is a more critical priority today than it was a few years ago, yet only 18% of ERM leaders express high confidence in identifying and managing emerging risks.

The mid-market model has a structural advantage: every risk has a named owner who sits on or near the executive team. The path from risk identification to executive decision is one or two hops, not five. When the customer concentration risk moves, the executive who owns it is in the room when the CFO sees the update.

This is what strategic risk management is supposed to do. Fortune 500 programs achieve it through infrastructure. Mid-market programs achieve it through proximity.

Key Takeaways

- Strategic risk management for mid-market companies is a different operating model from the Fortune 500 version, not a smaller version. The bottleneck at the mid-market level is executive time, not framework sophistication.

- An effective mid-market program has three properties: a short list of 20 to 40 named strategic risks, one designated owner per risk, and a quarterly cadence integrated into the existing finance operating rhythm.

- The CFO role in risk management at the mid-market level is integration, not ownership. The CFO consolidates owner updates into a one-page report for the audit committee, while each risk has a single named executive accountable for it.

- Concrete strategic risk management examples at the mid-market level look like customer concentration owned by the CRO, regulatory exposure owned by the GC, and cyber breach owned by the CIO. Named risk, named owner, quarterly update.

- The mid-market model produces faster risk-informed decision making than Fortune 500 programs because the path from risk identification to executive decision is one or two hops, not five.

The buying lesson

If a firm is pitching you strategic risk management built around a CRO function, a risk committee structure, and a quantitative risk modeling layer, ask whether you have the headcount to absorb it. If you do not, you are buying infrastructure for a company you are not.

You do not need a Fortune 500 strategic risk management program. You need a short list of named risks, one owner per risk, a quarterly cadence, and a one-page report. That is the model that produces decisions.

Frequently Asked Questions

What is strategic risk management for a mid-market company?

Strategic risk management is the discipline of identifying the risks that could prevent the company from achieving its strategy, owning them at the executive level, monitoring them on a known cadence, and escalating them when they move. For a mid-market company specifically, it is a different operating model from the Fortune 500 version: a short list of 20 to 40 named risks, one designated owner per risk, and a quarterly cadence integrated into the existing finance operating rhythm. It does not require a CRO function or a board risk committee.

What is a good example of strategic risk management at the mid-market level?

A $200M industrial distributor with customer concentration is a clear example. The top three accounts represent 47% of revenue. The strategic risk is named 'Concentration in top three accounts,' owned by the Chief Revenue Officer. Each quarter the CRO reports concentration percentage, account health changes, and diversification actions. The CFO consolidates this into a single line for the audit committee. One named risk, one named owner, one quarterly update, one decision-ready report line for the board.

What is the CFO role in risk management at a mid-market company?

The mid-market CFO's role in risk management is integration, not ownership. The CFO does not own every strategic risk personally. Each risk has a single named executive owner. What the CFO owns is the consolidation: making sure risk owner updates feed into the existing finance review cycle, ensuring the audit committee receives one consolidated risk report inside the standard audit committee package, and connecting strategic risk management to the broader enterprise risk management framework that includes operational, compliance, and internal audit findings.

How does mid-market strategic risk management differ from enterprise risk management?

Enterprise risk management is the broader framework that covers strategic, operational, compliance, and financial risks. Strategic risk management is the top layer focused specifically on risks to the company's strategy. At the Fortune 500 level, these are often separate workstreams owned by separate teams. At the mid-market level, they share one risk register, one owner list, and one report. The integration is what makes the model work for companies that do not have the headcount for separate risk functions.