Risk Management

Vendor Risk Management Is a Financial Exposure Problem, Not a Procurement Problem

Mid-market companies treat vendor risk as a procurement checklist when the exposure sits squarely on the balance sheet. Here is how CFOs can reframe third-party risk as a financial discipline.

By Eric Kennedy · Fri May 01 2026 · 6 min read

Procurement teams are built to negotiate. They protect margin, enforce contract terms, and standardize vendor onboarding. What they're not built to do is quantify systemic financial exposure sitting quietly inside your third-party relationships, and that gap is costing mid-market organizations far more than a bad contract clause.

According to the IBM Cost of a Data Breach Report, data breaches initiated through a third-party vendor cost an average of $4.33 million, a figure that lands directly on the balance sheet, not in a procurement spreadsheet.

A vendor breach is no longer an IT problem. It's a financial exposure event.

The mid-market instinct is understandable: build a vendor onboarding checklist, collect a SOC 2 report, check the box. That process creates the feeling of control without the substance of it. Structured vendor risk management isn't a gatekeeping exercise, it's an ongoing financial discipline.

That distinction matters, and it's one most organizations don't confront until after the loss occurs.

The $4.33 Million Procurement Trap

Procurement-led vendor programs were designed for a world where the worst case was a missed delivery or a pricing dispute. That world no longer exists. Today, a single third-party failure can trigger regulatory disclosure obligations, customer churn, and a multi-million dollar hit to operating income.

The trap is structural: procurement is measured on cost savings and cycle time, not on continuous financial exposure. So vendor risk gets compressed into the moment of contract execution, then quietly dropped from the active management surface.

Why the 'Onboarding-Only' Model Fails the CFO

Most organizations treat vendor risk like a background check before a hire: run it once, file it away, and assume the situation stays static. It doesn't.

The moment a contract is signed, active risk management effectively stops in most procurement-led programs. Questionnaires get completed, boxes get checked, and vendors move into production. What follows is months or years of unchecked exposure.

This is the Procurement Gap: due diligence performed at the point of sale tells you who a vendor was, not who they are today.

Three failure points define this model:

- Periodic reviews replace continuous monitoring. Annual assessments can't catch a vendor's deteriorating financial position or a mid-year regulatory violation.

- GRC frameworks stop at the RFP stage. Governance, risk, and compliance obligations don't end at vendor selection, they run the full contract lifecycle.

- Concentration risk compounds silently. As vendor relationships deepen, dependency grows in ways no onboarding checklist can anticipate.

Third-party risk is a lifecycle issue, not a gatekeeping issue. Treating it otherwise is where financial exposure quietly builds.

According to Gartner, the majority of organizations identify material third-party risks after the initial onboarding and due diligence phase, confirming that the moment of greatest control is rarely the moment of greatest risk.

That exposure doesn't arrive as a single event. It accumulates across four distinct categories, each carrying its own financial consequence for the organization.

The 4 Pillars of Financial Exposure in VRM

Before your finance team can quantify vendor risk, they need to know what form it takes.

The four pillars of vendor financial exposure. Each carries its own consequence to the balance sheet.

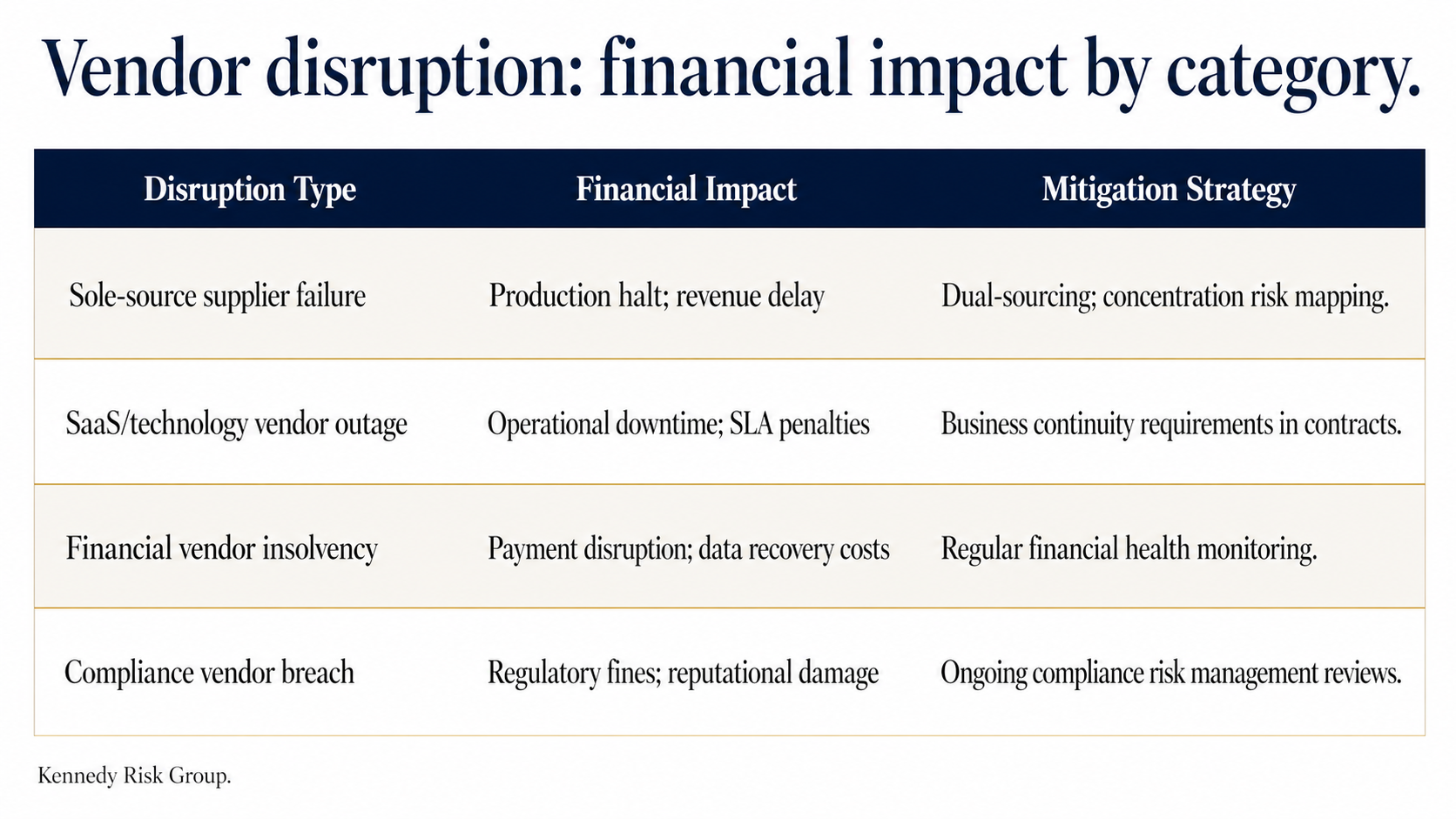

Strategic Risk

This is what happens when a critical vendor failure prevents you from executing on long-term growth objectives: a product launch delayed, a market entry stalled, a client contract lost. The damage isn't always immediate, but it compounds.

Operational Risk

Business continuity management breaks down the moment a key vendor goes dark without warning. Daily production, customer fulfillment, and service delivery don't pause while you source alternatives. Downtime is dollars.

Compliance and Legal Risk

Regulatory exposure carries a financial premium that most organizations underestimate until the fine lands. When a vendor mishandles data or violates sector-specific regulations, your organization often shares liability for the breach.

Reputational Risk

This one's harder to put a number on, and that's precisely why it's dangerous. A single high-profile vendor failure can erode brand equity, trigger investor scrutiny, and compress market cap in ways that outlast the original incident.

Understanding these four pillars isn't just a risk taxonomy exercise. It's the foundation for translating vendor exposure into the financial language your board and leadership team actually act on, which means examining what that volatility does to your bottom line.

How Vendor Volatility Erodes EBITDA and NOI

Supply chain disruptions aren't black swan events. They're predictable volatility that most finance leaders haven't built into their risk models.

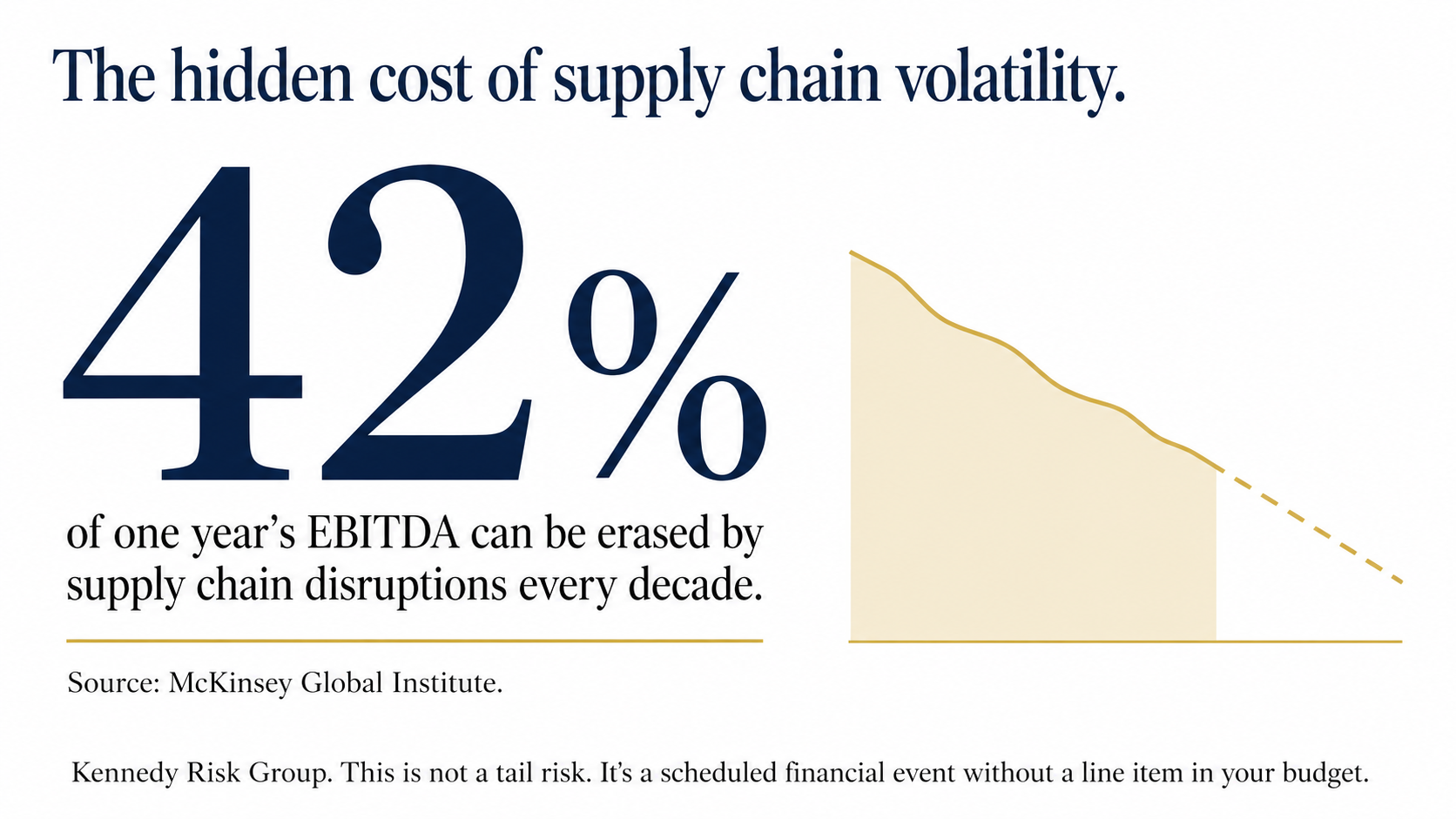

McKinsey Global Institute research puts this in stark terms: companies can expect supply chain disruptions to erase roughly 42% of one year's EBITDA every decade. That's not a tail risk. That's a scheduled financial event without a line item in your budget.

McKinsey Global Institute research puts this in stark terms: companies can expect supply chain disruptions to erase roughly 42% of one year's EBITDA every decade. That's not a tail risk. That's a scheduled financial event without a line item in your budget.

Vendor downtime doesn't stay in operations, it migrates directly to your income statement, compressing NOI in ways that are difficult to reverse quickly.

The link between vendor uptime and Net Operating Income is more direct than most CFOs account for. A critical SaaS vendor going offline for 72 hours, a sole-source supplier missing a production window, a payments processor experiencing an outage: each scenario creates cascading revenue delays, contractual penalties, and remediation costs that quietly shrink margins.

This is precisely where structured risk assessment services create measurable value. Quantifying the "Value at Risk" for your top vendors, treating them the same way treasury teams treat financial instruments, moves VRM from compliance checklist to capital protection.

That shift in approach is exactly what the next section addresses: how CFOs can build a forward-looking framework that makes this kind of exposure visible, manageable, and integrated into broader enterprise decision-making.

What CFO-Led Vendor Risk Management Looks Like

Four steps to move vendor risk from procurement checklist to CFO-led discipline.

Identifying the exposure is only half the work. The harder task is building a structure that catches problems before they hit the income statement. Here's a practical, four-step framework for finance leaders ready to take ownership of vendor risk.

- Move from annual reviews to continuous monitoring. Static questionnaires miss the volatility that exists between review cycles. Modern VRM frameworks emphasize real-time data feeds precisely because vendor financial health, operational capacity, and compliance standing can deteriorate in weeks, not quarters.

- Integrate third-party risk into your ERM dashboard. Vendor exposure shouldn't live in a procurement spreadsheet. It belongs alongside market risk, liquidity risk, and operational risk, visible to the CFO and the audit committee in one consolidated view.

- Model concentration risk explicitly. Ask the stress-test question directly: what happens if your top three vendors fail simultaneously? If the answer isn't documented, that's a material gap.

- Leverage risk assessment services to automate governance, risk and compliance workflows. Right-sized GRC automation reduces the manual burden on internal audit teams while improving coverage and consistency across your vendor portfolio.

Vendor risk isn't a one-time project, it's a recurring discipline that demands executive ownership. The question is whether your organization is set up to exercise it.

The Question to Ask Before Your Next Vendor Failure

Before the next vendor disruption hits your income statement, one question deserves a direct answer: Who owns this risk?

If the honest answer is "procurement," your balance sheet is exposed.

Vendor risk is a financial concentration risk. Procurement teams manage contracts and costs. They don't model EBITDA sensitivity to single-source dependencies or flag when a key supplier's financial deterioration is compressing your NOI. That requires a CFO-led mandate, one embedded in structured enterprise risk management, not a vendor scorecard spreadsheet.

Protecting the balance sheet means treating vendor volatility the way you'd treat any material financial exposure: with visibility, structure, and accountability at the executive level.

Kennedy Risk Group's ERM Diagnostic is built for exactly this conversation, giving mid-market finance and audit leaders a practical, right-sized assessment of where vendor concentration risk lives on their balance sheet and what it would take to contain it.

The cost of a vendor failure is always higher than the cost of anticipating one.

If you're ready to put a CFO-led structure around your vendor risk before the next disruption forces your hand, connect with Kennedy Risk Group to start your ERM Diagnostic.

Key Takeaways

- A vendor breach is no longer an IT problem. It's a financial exposure event with an average cost of $4.33 million.

- Procurement-led vendor risk management fails the CFO because due diligence is point-in-time while exposure is continuous.

- The four pillars of vendor financial exposure: strategic, operational, compliance and legal, and reputational risk.

- Supply chain disruptions can erase up to 42% of one year's EBITDA every decade. That's a scheduled event, not a tail risk.

- If procurement owns vendor risk, your balance sheet is exposed. The mandate belongs at the CFO level, integrated into ERM.

Frequently Asked Questions

Why is vendor risk management a CFO issue, not a procurement issue?

Procurement is measured on cost savings and cycle time, not on continuous financial exposure. Vendor failures land directly on the income statement and balance sheet through lost revenue, regulatory fines, and remediation costs, which makes vendor risk a financial concentration risk that belongs at the CFO level.

What is the average financial impact of a third-party vendor breach?

According to the IBM Cost of a Data Breach Report, breaches initiated through a third-party vendor cost an average of $4.33 million per incident. That cost reflects detection, response, regulatory exposure, and lost business, and it lands on the balance sheet rather than the procurement budget.

What are the four pillars of vendor financial exposure?

Strategic risk (delayed growth execution), operational risk (downtime and SLA penalties), compliance and legal risk (regulatory fines and shared liability), and reputational risk (brand erosion and market cap compression). Together they define where third-party exposure sits on the balance sheet.

How often should vendor risk be reassessed?

Continuously. Annual or onboarding-only reviews cannot catch a vendor's deteriorating financial position, mid-year regulatory violations, or growing concentration risk. Modern VRM frameworks rely on real-time monitoring of financial health, operational capacity, and compliance standing across the full contract lifecycle.

What is concentration risk in vendor management?

Concentration risk is the financial exposure that builds when too much operational dependency sits with a small number of vendors. It compounds silently as relationships deepen and is best surfaced through explicit stress tests, such as modeling the simultaneous failure of your top three vendors.