Internal Audit

The Strategic Pivot: From Compliance Cop to Business Advisor

Mid-market CFOs are transforming internal audit from a compliance exercise into a strategic intelligence function. Here is how governance risk and compliance consulting, co-sourcing, and board-ready reporting turn audit findings into funded priorities.

By Eric Kennedy · Tue Apr 14 2026 · 10 min read

For too long, internal audit has occupied an uncomfortable seat at the corporate table, respected enough to tolerate, but rarely invited into the conversations that actually shape strategy. That dynamic is changing fast, and mid-market CFOs who recognize the shift are turning internal audit services into one of their most powerful performance levers.

The traditional model is familiar: auditors arrive, tick boxes, flag exceptions, and file reports that collect dust until the next cycle. It is a reactive posture built for a simpler regulatory environment. Today's business landscape, with its layered compliance obligations, operational complexity, and accelerating risk, demands something fundamentally different.

Mid-market firms face a particular disadvantage here. Unlike large enterprises with dedicated centers of excellence, they often lack the internal bench strength to evolve their audit function organically. This is precisely why internal audit co-sourcing has gained significant traction: it gives growing companies access to specialized expertise without the overhead of a fully built-in-house team.

Strategic auditing transforms internal audit from a scorekeeper into a forward-looking advisor that actively strengthens business resilience.

Think of it less as a compliance function and more as an intelligence function, one that identifies inefficiencies, surfaces emerging risks, and informs executive decision-making in real time. However, making that transition requires more than goodwill. It demands a clear-eyed look at what "good enough" risk assessment is actually costing your organization.

The High Cost of 'Good Enough' Risk Assessment

Shifting from a reactive to a strategic audit posture sounds compelling in theory, but the urgency becomes undeniable when you examine what "good enough" risk assessment actually costs.

Non-compliance is not a single line item. It is a multiplier. Direct fines are only the visible tip: beneath the surface sit legal fees, remediation costs, operational disruption, and the reputational damage that quietly erodes customer trust and partner confidence. A mid-market company operating on tighter margins than its enterprise-scale competitors can absorb these compounding costs far less gracefully. What might be a manageable quarterly write-down for a Fortune 500 organization can be an existential event for a $200M business.

Compliance drift is an equally dangerous, and far more insidious, threat. It happens gradually: policies age without updates, control environments shift with personnel changes, and risk exposure quietly widens while leadership remains focused on growth. Regular risk assessment services exist precisely to interrupt this drift before it calcifies into systemic vulnerability. Think of it as scheduled maintenance versus emergency repair; the cost differential is rarely close.

This is where governance risk and compliance consulting earns its strategic value. Rather than simply cataloging what could go wrong, a disciplined consulting engagement identifies which risks genuinely threaten capital preservation, protecting the retained earnings and operating cash flow that fuel future growth initiatives.

Capital preservation is the quiet mandate behind every strong audit function. Protect what you have built, and growth becomes far less fragile.

Understanding how this framework connects to broader enterprise performance, and how an integrated approach can actually accelerate growth targets rather than constrain them, is exactly where the conversation needs to go next.

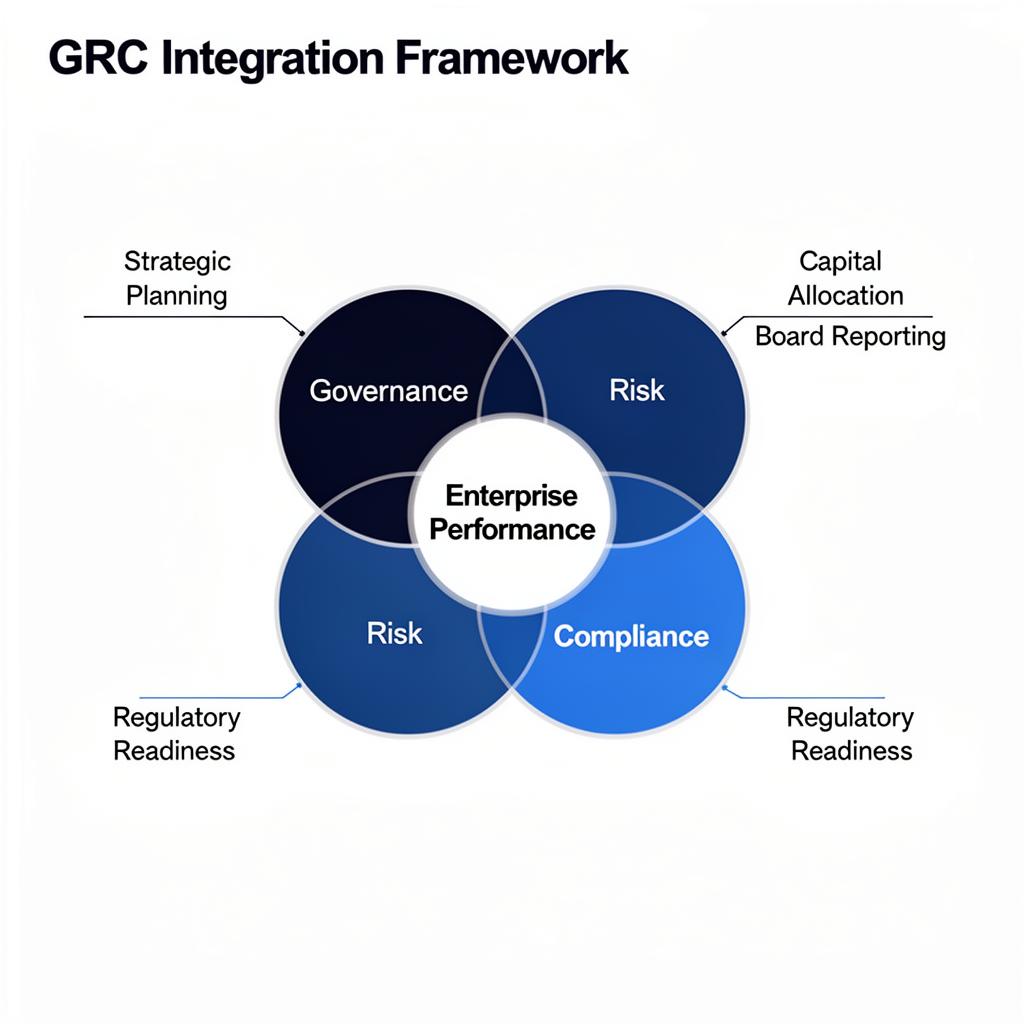

Integrating GRC into the Enterprise Performance Engine

The previous sections established why strategic audit thinking matters and what it costs to ignore it. Now comes the practical question: how do you actually wire governance, risk, and compliance into the machinery of business growth?

GRC (Governance, Risk, and Compliance) is not a compliance department initiative. At its core, GRC represents an integrated collection of capabilities designed to help organizations reliably achieve objectives, address uncertainty, and act with integrity. The moment a mid-market CFO treats these three disciplines as a unified performance system rather than separate administrative functions, the entire strategic conversation shifts.

From Checkboxes to Growth Enablers

An enterprise risk management framework does something counterintuitive: it makes aggressive growth targets more achievable, not more constrained. When leadership has clear visibility into risk appetite, resource exposure, and operational vulnerabilities, they can pursue expansion with confidence rather than hesitation. In practice, organizations that embed risk intelligence into strategic planning cycles identify threats earlier and allocate capital more decisively.

This is precisely where GRC consulting services create measurable value, translating complex risk data into board-ready insights that accelerate decision-making instead of slowing it down.

The Resilience Imperative

GRC thinking has undergone a fundamental shift. The old model prioritized readiness, building controls to pass audits. The emerging standard demands resilience, building systems that absorb disruption and adapt without losing momentum. This distinction matters enormously for mid-market companies operating with leaner teams and tighter margins.

How organizations close that resilience gap often comes down to who they bring into the room, and that question leads directly to a critical strategic choice about capability models.

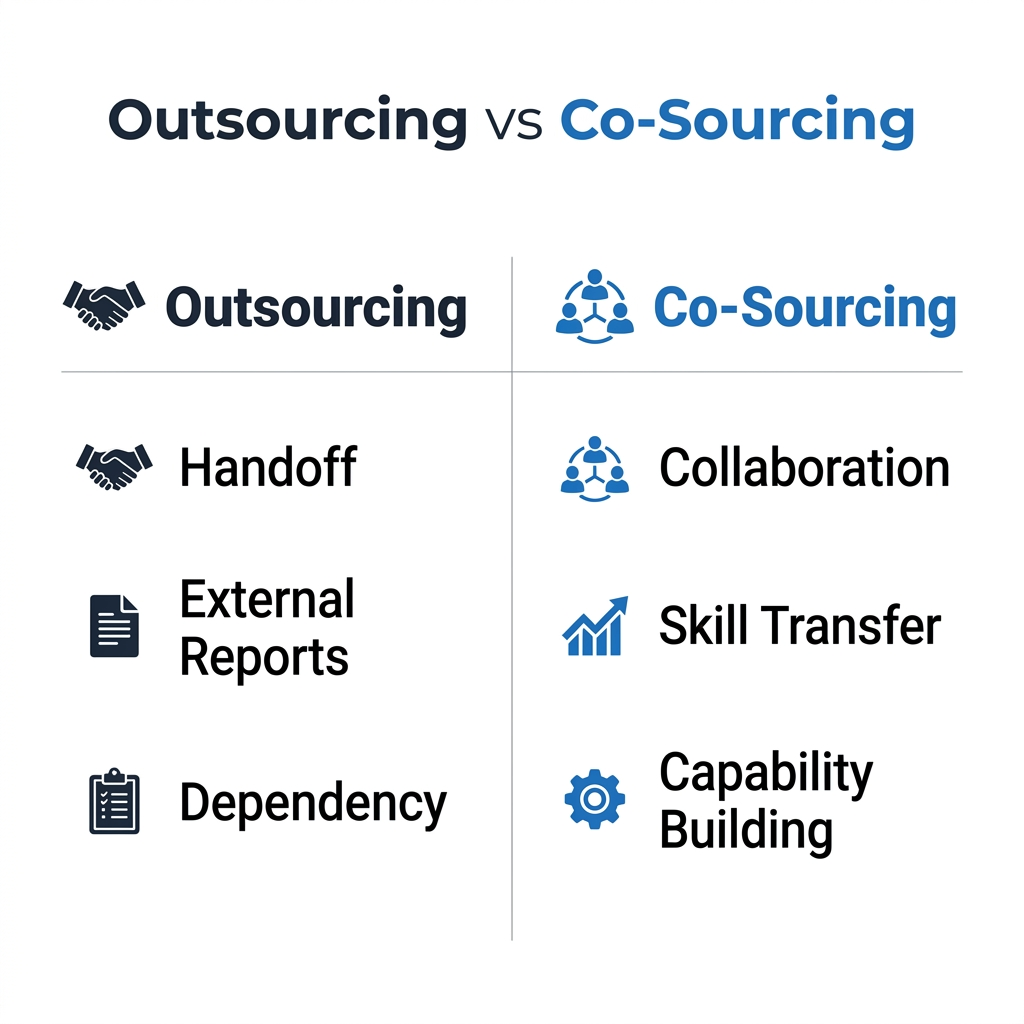

Co-Sourcing vs. Outsourcing: Building Long-Term Capability

With GRC now embedded in performance management, the next practical question for mid-market CFOs is who actually does the work. Not every organization can staff a full internal audit function with deep expertise across every risk domain, and that is where the choice between outsourcing and co-sourcing becomes strategically significant.

The Difference Between Hands-Off and Hands-On

Traditional outsourcing transfers audit responsibilities to an external provider entirely. The vendor delivers findings, and your team receives a report. It is efficient on paper, but it creates a dependency problem: institutional knowledge walks out the door with the engagement, and your internal team learns very little in the process.

Co-sourcing works differently. It is a collaborative model where external specialists work alongside your internal team, sharing methodology, transferring skills, and building capability with every engagement. Rather than replacing your people, co-sourcing multiplies them.

A strong internal audit function is not built in a single engagement; it is built through every engagement.

Closing the Expertise Gap

This distinction matters most in high-complexity areas where specialized knowledge is non-negotiable. Cybersecurity audits, ESG compliance reviews, and advanced risk assessment services all require niche expertise that is difficult, and expensive, to hire full-time at the mid-market level. Co-sourcing gives CFOs on-demand access to that expertise without the permanent overhead.

According to Internal Auditing Around the World, top-performing audit functions consistently blend internal resources with external specialists to address evolving risk landscapes.

Building Capability, Not Just Coverage

The long-term payoff of co-sourcing is institutional. External partners coach internal staff on frameworks, documentation standards, and emerging risk methodologies. Over time, your team absorbs that knowledge, reducing external dependency while raising overall audit maturity.

That maturing capability becomes especially valuable when it is time to communicate audit results upward. Which raises an important question: once your team has produced rigorous, high-quality findings, how do you translate that work into language that resonates in the boardroom?

From Audit Findings to Boardroom Action

Once the right talent model is in place, whether co-sourced or otherwise, the real test is what happens with the output. Too often, technically sound audit findings get buried in dense reports that boards never meaningfully engage with. Translating that work into boardroom-ready communication is where risk and compliance consulting expertise pays its most visible dividend.

The core challenge is translation. Auditors speak in control gaps and process deficiencies; boards need to hear about strategic risk exposure, financial impact, and decisions required. A practical approach is to map every significant finding to a business objective it threatens: cost, growth, regulatory standing, or reputation.

Structured board meeting agendas and documented minutes also matter more than most CFOs realize. They serve as formal evidence of duty of care, demonstrating that leadership actively reviewed and responded to risk information, which is critical protection in litigation or regulatory scrutiny.

A straightforward roadmap for CFOs:

- Summarize findings in plain language with dollar-range impact estimates

- Prioritize issues by likelihood and consequence, not audit severity alone

- Assign ownership and remediation timelines before the meeting, not during it

- Track progress at each subsequent board session to close the loop

The board's job is not to understand audit mechanics; it is to make informed decisions. Your job is to make that effortless.

When CFOs master this translation layer, audit stops feeling like a compliance obligation and starts functioning as a genuine governance asset, which sets the stage for a broader conversation about what that means for the organization's future.

Conclusion: Securing Your Organization's Future

Internal audit is not a compliance tax; it is a performance driver that, when structured correctly, feeds better decisions at every level of the organization. The sections above show a clear pattern: mid-market companies that embed an enterprise risk management framework into day-to-day operations, rather than treating it as a periodic event, consistently convert audit findings into boardroom action faster and more effectively.

A well-resourced, co-sourced GRC model gives CFOs something no checklist ever could: forward-looking visibility.

Key takeaways to carry forward:

- Audit function design determines strategic value, not just compliance coverage

- Co-sourcing builds internal capability while delivering specialized expertise

- Board-ready reporting transforms findings into funded priorities

- GRC integration turns risk management into a performance input, not an afterthought

The shift will not happen overnight, but the direction is clear. Organizations ready to move beyond the checklist mentality, toward integrated, intelligence-driven audit functions, will be better positioned to grow, adapt, and protect stakeholder value.

If this approach resonates, explore how Kennedy Risk Group structures integrated risk management for mid-market organizations. The conversation is worth having before your next audit cycle begins.

Frequently Asked Questions

What is the difference between internal audit outsourcing and co-sourcing?

Outsourcing transfers audit responsibilities entirely to an external provider, creating dependency and limited knowledge transfer. Co-sourcing is a collaborative model where external specialists work alongside your internal team, sharing methodology, transferring skills, and building lasting capability with every engagement.

How do internal audit services create strategic value for mid-market companies?

Strategic internal audit moves beyond box-checking to function as an intelligence asset. It identifies inefficiencies, surfaces emerging risks, and informs executive decision-making in real time, helping leadership pursue growth with confidence while protecting capital and retained earnings.

What does governance risk and compliance (GRC) consulting involve?

GRC consulting integrates governance, risk management, and compliance into a unified performance system. It translates complex risk data into board-ready insights, embeds risk intelligence into strategic planning cycles, and builds organizational resilience rather than just regulatory readiness.

How should CFOs communicate audit findings to the board?

Map every significant finding to a business objective it threatens, such as cost, growth, regulatory standing, or reputation. Summarize findings in plain language with dollar-range impact estimates, prioritize by likelihood and consequence, assign ownership and remediation timelines before the meeting, and track progress at each subsequent board session.

Why is risk assessment important for mid-market organizations?

Mid-market companies operate on tighter margins than enterprise-scale competitors. Regular risk assessment services interrupt compliance drift before it becomes systemic vulnerability, protect capital preservation, and ensure that risk exposure does not quietly widen while leadership focuses on growth.